- Key Takeaways

- The Unique Blended Family Dilemma

- Key Blended Family Estate Planning Strategies

- Beyond Money: The Human Element

- Choosing Your Fiduciaries Wisely

- Why Communication is Non-Negotiable

- When to Update Your Plan

- Conclusion

- Frequently Asked Questions

- How is estate planning different for blended families?

- What key documents should a blended family have in place?

- How can trusts help in a blended family estate plan?

- How do I choose the right executor or trustee for a blended family?

- Why is communication so important for blended family estate planning?

- When should a blended family update its estate plan?

- How can we avoid conflict between stepchildren and a surviving spouse?

Key Takeaways

- Blended family estate planning introduces unique risks of conflict among spouses, ex-spouses, biological children and stepchildren, so a clear and comprehensive plan is paramount to avoid disputes and unintended consequences. Begin by laying out your entire family tree and discussing priorities for spouse support and children’s inheritance.

- The friction between caring for a surviving spouse and safeguarding children’s shares can be minimized with detailed wills, clever trusts, and clear instructions that delineate who gets what and when. Make a list of important assets and the way you want to divide these assets between your spouse and each child.

- Accidental disinheritance occurs when wills, joint ownership, and beneficiary designations are not changed after divorce, remarriage, or new births. Ensure you review all policies, accounts, and legal documentation every time your family or finances shift. Don’t depend solely on default provincial legislation.

- Past commitments like alimony, child support, or settlements from previous relationships can supersede or interfere with your present desires. Bring in all court orders and legal agreements to review with someone competent so your estate plan fully honors these obligations and no claims arise down the road.

- Beyond cash, these choices about keepsakes, guardianship and who counts as “family” can powerfully shape long-term peace in a blended family. Keep the lines of communication open, put down in writing exact wishes for personal possessions and guardianship, and specify who you consider part of your family in your plan.

- Selecting the right executors, trustees, and agents is especially important in a blended family, as these individuals will implement your plan and control disputes. Think neutral or professional fiduciaries where relationships are acrimonious, and provide them clear written direction to follow if you become incapacitated or post mortem.

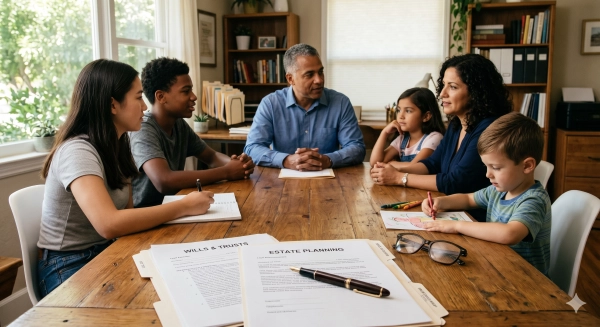

Blended family estate planning is figuring out how money, property, and care will pass to children, stepchildren, and the new spouse in a second or later marriage. In many blended homes, partners have kids, assets, and debt from previous relationships that can cause holes if a plan is not in place. Some of the typical problems are how to divide a home, treat kids equally, and shield a new spouse without disinheriting the kids from a prior marriage. Wills, trusts, and beneficiary forms frequently require specific provisions in blended families. To provide a clear foundation, the following sections discuss main strategies, critical decisions, and pitfalls to avoid in blended family planning.

The Unique Blended Family Dilemma

Blended family estate planning has a lot more moving pieces than your standard one-household, first-marriage plan. There might be multiple children, stepchildren, ex-wives, husbands, girlfriends, and boyfriends who all have their own legal rights and expectations. With nearly one in eight couple families with children now a blended one, these types of challenges are no longer isolated fringe events. Without a plan, estate law rules can crash into family dynamics and generate stress, mistrust, and expensive legal battles.

In Alberta, the Wills and Succession Act and the Family Property Act inject additional complexity. A second marriage, divorce, or newborn can alter how a will operates, who can request support from the estate, and if an old vow still applies. What seems “fair” at the beginning of a new marriage might not suit 10 years later when relationships have changed or assets have increased. A specific, updated plan is crucial to prevent no one getting what they wanted, whether it be stepkids disinherited or a widowed spouse with too little.

The Spouse vs. Child Conflict

In blended families, one of the toughest challenges is embracing a widow or widower while maintaining a transparent track for their kids from previous marriages. An ‘everything to my spouse’ will might seem straightforward, but after the first spouse passes away, the survivor is free to rewrite their own will to benefit only their biological children, a new spouse, or charity and leave stepchildren out in the cold. When the will and trust terms are ambiguous, each side can interpret them to attack the other, transforming grief into legal warfare. To mitigate that risk, remarried couples frequently use trust arrangements where a spouse can access assets in life, while the principal later passes to kids from the first marriage. It’s a tricky balancing act, balancing the spouse’s right to live with dignity and security with the children’s expectation that they’ll get at least some portion.

A simple way to bring clarity is to write down a specific split between spouse and children. For example:

- Spouse: Right to live in the family home for life.

- Children: ownership of the home after spouse’s death

- Spouse: income from investment portfolio

- Children: the portfolio capital, divided equally

- Stepchildren: either a set cash gift or a set share of the estate.

Accidental Disinheritance

The standard danger is inadvertent disinheritance when papers get jammed in a previous chapter of life. Or maybe they remarry, but neglect to update an old will or a life insurance form that still lists an ex-spouse. Joint ownership and “pay on death” designations can bypass the will entirely, directing assets directly to the co‑owner or named individual and leaving nothing in the estate for other kids. When that happens, the law tracks the paperwork, not the original intent. Depending solely on Alberta’s default rules can come as a surprise since the legislation centers on legal spouses and dependent family members and may not align with what a blended family had in mind. Review wills, beneficiary designations and titles after any big change like divorce, remarriage, a new child or the purchase of a major asset.

Unspoken Expectations

A lot of blended families operate with unspoken understandings about who “will of course” receive what. Parents think adult children understand that a new spouse will be taken care of first and then whatever filters down. Kids might take for granted that old family assets, such as a business or land, will forever remain on their side of the family. If no one says these things out loud, those private beliefs collide after a death and can rapidly turn into resentment.

Discussing the plan with all involved family members helps reduce anxiety and uncertainty. It further forces fuzzy concepts into some real decisions, such as whether stepchildren should receive the same portion as biological children or a different one. To alleviate hurt feelings, it helps to note down who should get what—heirlooms, tools, art, etc.—there is less pain when people know a decision was made, rather than left to chance. Verbal promises, however heartfelt, are difficult to demonstrate and easy to challenge, and therefore ought to be supported by directions in a will or memorandum.

Previous Obligations

Blended family planning must honor financial commitments from previous relationships. These typically consist of court-ordered child support, spousal support, or equalization payments under property laws. If those obligations aren’t considered by the estate plan, the estate might not have sufficient funds to satisfy old obligations and new desires. A definitive inventory of any existing payments, warranties, or separation agreement clauses assists in demonstrating what has to be paid off prior to anything being dispersed among heirs.

These previous entitlements can grant ex-spouses or minor children a legal right to stake a claim against the estate if they are not covered. Pretending like they don’t exist doesn’t make them go away. It simply moves the issue into the courtroom and possibly depletes the estate with legal fees.

Key Blended Family Estate Planning Strategies

Not surprisingly, blended families usually require more than one weapon in their estate planning arsenal to protect everyone equally. A good plan typically blends wills, trusts, beneficiary forms, and marital agreements, and then gets reviewed frequently as people age, remarry, move, or change jobs.

1. Precise Wills

A transparent will is the foundation. It should describe, in clear terms, who inherits what, when, and in what proportion, including stepchildren, adopted children, and kids from previous relationships. These are the details generic or template wills tend to gloss over, which can ultimately push your family into court or compel them to adhere to default inheritance laws.

Name each non-biological child you want to include as a beneficiary. Even a line like “all my children” may not include stepchildren in certain jurisdictions. Specific bequests, like “EUR 50 000 to my stepdaughter Ana,” reduce ambiguity and emotional pain. Include contingent beneficiaries so things still function if someone passes first or disclaims.

- Don’t die intestate. Update your will if you remarry. In some parts of the country, marriage can revoke an old will. A neutral third-party executor, such as a trusted adviser or a professional, can reduce the chances of friction between a new spouse and adult children.

2. Strategic Trusts

Trusts can divide control longitudinally. For instance, a spousal trust could provide your current spouse income for life while the trust retains the principal for your kids after that spouse passes away. A joint partner trust or life insurance trust will hold larger accounts so they bypass probate and move in a more private, controlled way.

For example, you can set rules on the timing and size of payouts, like staged payments at ages 25, 30, and 35, or limiting payouts to certain conditions like health or education. This serves to shield minor or otherwise vulnerable family members from abuse, creditors, or new spouses. In certain structures, a trust funded at the first spouse’s passing can maintain those assets apart from the surviving spouse’s estate, potentially protecting them from subsequent claims. Tax rules vary widely, and bad drafting can trigger additional tax on the first spouse’s death, so local legal and tax advice is important.

3. Beneficiary Designations

A lot of assets, such as life insurance, retirement funds, and some investment or registered accounts, pass by beneficiary form, not will. After a new marriage or new children, these forms should be reviewed and, if necessary, updated to align with your will and trust strategy.

Direct designations can deliver funds immediately to a spouse, child, or trust without having to wait for probate. That can help cover living expenses or final expenses while the remainder of the estate is being settled. A straightforward table noting each account, institution, account number, and named beneficiaries simplifies the task for your executor and reduces the risk that an old ex-partner or outdated designation is still on file.

If local law gives a surviving spouse robust rights, for example, a claim for a jure share of family property or support, ensure the blend of designations, trusts, and will still conform to those rules and your objectives.

4. Marital Agreements

A marital agreement—whether a prenup, postnup or cohabitation contract—can define what assets remain “yours,” what is “ours” and what each partner would like to leave to children from previous marriages. This helps establish reasonable expectations and can minimize disputes if the relationship dissolves by death or divorce.

They can anticipate potential claims by a former spouse or stepchildren and may reference a prenuptial agreement that dictates how assets are divided. In certain blended plans, spouses even sign a side agreement agreeing not to alter their wills after a spouse passes away so that the kids on both sides retain the inheritance they agreed upon. As jobs, savings, and family roles change, these contracts need to be revisited and, if necessary, revised.

5. Powers of Attorney

Powers of attorney are used to name individuals to make decisions regarding money, property, or health in case you are unable to do so yourself. With blended families, it might be smart to select someone neutral or a spouse with an adult child and specifically designate who handles what to minimize conflict.

Written directions could address support of a current spouse, support of children from prior relationships, and gifts or loans to relatives. Alternate agents keep the plan moving if the first pick is sick, out of the country, or hesitant to act. These documents should be reviewed when trust shifts, new partners appear, or key individuals relocate.

Beyond Money: The Human Element

Estate planning in a blended family isn’t just about who receives what money. It queries how you desire the people you love to connect with one another once you are no longer around. Because families function as systems, a difficult decision for one member reverberates throughout the group, and minor resentments can fester into protracted feuds if they aren’t nipped in the bud.

Money alone can stress them. Studies connect money fights to a disproportionate share of divorces. Stepfamilies frequently enter the picture with money stress already part of the equation. Conflicting values on saving, spending, or assisting adult children can collide, particularly when blood runs deeper and more instinctual than fresh step-relations. When expectations are unrealistically high or when folks are praying a stepfamily will be a first family from the get-go, early hiccups can feel like flops instead of adjustment.

Writing down those non-monetary wishes provides more clarity for everyone. Documented advice on heirlooms, custodianship, and your definition of ‘family’ provides a soothing balm when emotions are apt to flare. It helps external advisers, such as lawyers or financial planners, avoid projecting their own opinions about how money “should” be used and instead remain focused on your real priorities.

Sentimental Items

The sentimental value of an object can mean more than well-padded bank accounts. A watch from a grandfather, a wedding china set, or old photographs from a first marriage can inspire powerful emotions about allegiance, heritage, and “ownership.” Biological bonds do render some things off-limits to stepchildren, no matter what the legal estate stipulates.

Identifying who should get crucial things and why can avoid squabbles. Discuss with adult children, stepchildren, and your spouse what items are most important to them and listen for underlying friction. These early, open conversations help lessen shame, blame, and the sort of finger-pointing that closes off communication and ensnares families in decades-long cycles of resentment.

- Wedding ring set → adult child from first marriage

- Grandparent’s old cooking pot is shared by everyone’s kid in turn.

- Family photo albums lead to digital versions for every branch of the family.

- Cultural and religious aspects involve individuals who are most engaged in those traditions.

Guardianship Choices

Guardianship decisions are frequently the most delicate subject in blended families — particularly when there are kids from multiple relationships. If you have minor or dependent children, naming guardians in your will can keep courts from imposing decisions that don’t take into account the specific subtleties of your family life. It mitigates the risk that an ex-spouse, a new partner and grandparents are all tugging in different directions simultaneously.

Emotions can flare when biological parents, stepparents, and extended family view themselves as “the best” caregiver. Family systems theory points out that systems resist change, so moving care from one home to another can feel threatening. Slow, open talks allow everyone to orient and shift from fright to fixing.

- Child’s current bond with each adult

- Willingness and long-term capacity of the proposed guardian

- Values on education, faith, culture, and discipline

- Capacity and resources to nurture all children at home.

- Plan for siblings and stepsiblings to keep regular contact

Defining “Family”

In a blended estate plan, ‘family’ isn’t a straightforward term. It’s for bio kids, the stepkids you raised, half siblings across multiple households and even chosen family or partners. Documents should reflect your actual situation, not a one-size-fits-all legal form that presumes a single husband and two kids.

Explicit communication about who is and is not a beneficiary prevents dashed hopes, particularly where biological and step ties intertwine. It lessens the danger that shame or harsh words will sweep in to supplant calm talks when folks view the ultimate paperwork. As marriages, divorces, and births change the structure of your family, refresh these definitions so the courts and your beneficiaries aren’t operating off of an outdated blueprint.

Choosing Your Fiduciaries Wisely

These are the individuals or institutions that execute your estate plan and poor choices can transform what was a blended family plan into a breeding ground of mistrust and conflict. Each role requires not only technical expertise but some level of emotional detachment from the family drama. In our experience, a combination of family members and professional fiduciaries is best, supported by transparent documentation, communication, and periodic review to ensure compliance with changing relationships and laws.

The Executor Role

Think of your executor as the person who has to run your will through the mill after you’ve died — someone who has to orchestrate paperwork and people simultaneously. In a blended family, that usually means a current spouse, ex-partner, and kids from different marriages, all with competing expectations. Anyone who already has conflict or takes sides in family disputes is a bad choice.

In Alberta, your executor needs to navigate local probate rules and estate law or face delays and court involvement. If the will is ambiguous or, even more problematic, there’s no proper will, provincial law can allocate the assets in a way that might not coincide with your intentions for your spouse, stepchildren, or children from a previous marriage. A lawyer who understands provincial rules could assist your executor in understanding duties, deadlines, and tax issues.

Written instructions go a long way toward minimizing disagreements. These can include how to pay off debts, how to distribute sentimental personal belongings among different sides of the family, and when to sell or retain jointly owned property. It’s a good idea to name one or two alternates should your first choice be unable or unwilling to serve when the time comes.

Family meetings can help vet your executor choice. If a suggested executor causes everyone to become tense or defensive, that’s valuable information. In certain higher-conflict blended families, a professional executor may be safer than any one relative.

The Trustee Role

A trustee handles assets within a trust. This is typical for blended families when you want to provide for a surviving spouse but shield inheritances for children from previous unions. This role can span years, so you need someone patient with some financial fluency and the wherewithal to say ‘no’ when demands fall outside the trust terms.

Trusts can go part way towards determining if and when children or stepchildren get funds and can manage cross-border or business assets. Trust structures need to be carefully drafted to avoid unintended tax consequences, particularly if beneficiaries reside in other provinces or countries. The trustee needs to know investment risk, family income needs and reporting requirements to tax authorities.

The trust document should spell out powers and limits in plain language: when the trustee may pay income or capital, when they should hold back funds, how to treat a second spouse versus adult children, and how to handle education costs or medical needs. This level of detail leaves less room for disagreement and provides the trustee with something objective to reference when decisions are not popular.

Regular reporting is key in blended families. Planned statements and easy digests of decisions assist in maintaining everyone informed and decrease suspicion. When assets are large or the family dynamic is already tenuous, a corporate trustee or professional trust company can serve as an impartial third party. That price can be counterbalanced by less conflict and more consistency in administration.

Trusts and other estate plans should be updated every few years or following major life transitions such as a new marriage, birth, or move to another province because estate and tax rules shift.

The Agent Role

An agent under POA acts while you’re still living but incapacitated. This could be finances, health care, or both. In a blended family, this role can be more fraught than executor or trustee as decisions regarding medical care or support for a current spouse versus adult children can incite strong emotions.

Should be clearly defined and limited so as not to be abused. Your paper can impose restrictions on big gifts, beneficiary designation changes, or support for family members, and it can mandate that the agent seek input from specific relatives or experts. Your agent should be wise, composed in a crisis, and capable of communicating complex decisions in layman’s terms to each family branch.

Open communication supported by instruments such as a prenup or marital agreement can help you align a new spouse and stepkids’ expectations long before tragedy strikes. Local law comes into play here because power of attorney and health directive rules vary by province or territory and influence what your agent is able to do or not.

| Agent Type | Scope of Authority | Key Selection Criteria |

|---|---|---|

| Financial agent (property/financial power of attorney) | Manage bank accounts, pay bills, handle taxes, oversee business interests within defined limits | Strong money sense, no debt or addiction issues, neutral toward all beneficiaries |

| Health care agent (health directive / personal directive) | Consent to treatment, choose care facilities, follow stated medical wishes | Respects your values, can speak clearly with medical staff, stable under pressure |

| Combined agent (both roles, where allowed) | Both financial and health decisions if permitted by local law | High integrity, time to serve, trusted by both spouse and children |

| Professional agent (lawyer, trust company, or other professional) | Focus on financial matters within contract terms | Useful when family conflict is high or assets are complex |

Why Communication is Non-Negotiable

Communication in a blended family estate plan is far more than a “nice to have.” It is the primary instrument that keeps everyone aligned and reduces the potential for extended disputes over finances, assets, or authority to decide. When multiple households, stepchildren, new partners, and ex-partners are in the mix, unspoken presumptions about what is “fair” can erupt into actual battles that span years.

Open conversations about your estate plans establish clear expectations. Each person may have a different picture of what should happen after a death: equal shares for all children, extra help for a child with health needs, or more support for a younger partner who still has a mortgage to pay. If these concepts remain under wraps, relatives could be blindsided or feel backstabbed when they observe the completed strategy. When you describe the plan in an open way, welcoming questions and keeping your tone respectful and non-judgmental, people can respond, request background, and express concerns early when adjustment is still easy.

Communicating the “why” behind important decisions frequently is just as important as the decisions themselves. For example, you may want to bequeath a bigger portion to a child that operates the business or establish a trust for stepchildren versus a straight gift. If you justify with reasons like need, age or previous support, family members will be less likely to project bias onto the plan. This type of clear communication helps preserve peace within the family and reduces the likelihood that one of them will later question the plan.

Recording what you talk about injects structure into these conversations. Brief records of what was decided, who acts as executor, or how a property should be used can remind all parties what was agreed to, especially when years go by and memories become fuzzy. Annual family check-ins keep the plan grounded in reality as jobs, homes, and relationships shift. This consistent, transparent communication facilitates an easier exchange of resources and alleviates tension all around.

When to Update Your Plan

Estate planning for a blended family isn’t a once and done situation. It needs fresh eyes as your life, assets, and local laws change so your plan still does what you meant it to do.

When should you update your blended family estate plan? Remarriage is a touchstone for blended families. In certain jurisdictions, such as Alberta, a new marriage can impact whether an old will remains valid. If someone remarries and does not make a new will, they may be considered to have died intestate, meaning the intestacy laws determine who inherits. That can shove most of the estate to the new wife and leave kids from a previous marriage short of what’s intended or even nothing. Divorce counts. You might not want an ex-spouse serving as executor or attorney under a power of attorney or key beneficiary anymore. The birth or adoption of a child or stepchild is another obvious trigger. Without an update, a younger child could be left out of the will, life insurance, or guardianship schemes. The death of a previous spouse, parent, or named guardian is another occasion to check in, as the previous beneficiaries in your plan may no longer be appropriate.

Update estate planning documents if there have been changes to any assets, beneficiaries, or family members. When to Update Your Plan Over 10 years your assets can shift a lot. You might sell a home, launch a business, shut down an account, or shift savings into a trust. If the will still has an old house or a closed account for a child, that child might be left holding the bag. In a blended family, this can stoke allegations of inequity. As the family dynamic evolves, you may want to drift from simple “equal shares” to a blend of lifetime support for a spouse and protected shares for kids from a prior marriage. A surviving spouse may be entitled to a portion of the estate, commonly one‑third to one‑half, if they receive insufficient under the plan. If your existing papers leave a new spouse too little, they may later make a legal claim, which can eat into what children get and spark strife. Updating beneficiary forms on your pensions, life insurance, and investment accounts is just as crucial as updating your will because those forms generally override the will with respect to who receives that money.

Keep an eye on legal and tax changes in Alberta that could affect the efficacy of your estate plan. Wills laws, family property laws, and dependant support laws do change. What worked with old rules might not work later. For instance, new regulations may prioritize claims by adult children or a spouse who was under-supported. Tax rules may switch the savvy from holding assets in one person’s name to using a trust or giving gifts during life. For blended families, these shifts can alter which child or branch of the family bears more tax burden. Routine legal checkups can help catch these gaps, like a trust that no longer complies with new laws or a will that no longer conforms with state property law.

Save a recurring reminder to review your estate plan every few years. Most advisers recommend a complete review every few years, even if nothing major has occurred, and at a minimum every decade your will typically requires another glance. What seemed equitable at the outset of a new marriage can appear drastically different after 10 years living together, more kids, or income changes. A simple calendar reminder or digital note can prompt you to pull out the documents and ask: Is everyone I care about still named? Are the shares still what I intend? Do my guardians, executors, and trustees still apply? Ongoing, easy check-ins prevent harsh outcomes such as a child being disinherited, a stepchild receiving more or less than intended, or a surviving spouse dragged into court to pursue essential support.

Conclusion

Blended family estate planning can be crushing. It doesn’t have to remain that way. With a plan in place, your kids, stepkids, and partner all get more peace and less wondering.

You experienced firsthand how trusts, clear wills, and a smart choice of guardians and trustees determine real outcomes. Simple conversations, done early enough, minimize surprise and pain down the road. A brief conversation today can save your family a lifelong battle tomorrow.

Things move quick in blended families. New jobs, new homes, divorce, or a new baby all shift the landscape.

To take action, consult an experienced estate attorney, document your objectives, and schedule a time to review your plan annually.

Frequently Asked Questions

How is estate planning different for blended families?

Blended family estate planning has to weigh a spouse’s needs with children from previous relationships. Absent explicit documents, local law may lean in favor of the live-in spouse or biological children. A personalized plan avoids dispute, minimizes tax problems, and ensures that all are cared for as desired.

What key documents should a blended family have in place?

Nearly all blended families require a will, powers of attorney, directives for healthcare, updated beneficiary designations, and frequently, a trust. These papers define who gets what, who makes decisions if you’re incapacitated, and how you protect both your spouse and kids for the long-haul.

How can trusts help in a blended family estate plan?

Trusts can provide for a surviving spouse and still preserve assets for children. They permit detailed rules, protect minors, and can cut down on fighting. Properly drafted trusts provide the structure, control, and flexibility that a simple will often cannot.

How do I choose the right executor or trustee for a blended family?

Select somebody neutral and organized, somebody who is trusted by both sides, not just one branch of the family. Think of a professional if tensions run high. A good executor or trustee can carry out your wishes, maintain records, and minimize family tension.

Why is communication so important for blended family estate planning?

Open communication guides expectations and minimizes surprises. When spouses and adult children know why your plan exists, there’s less opportunity for hurt feelings or legal battles. Transparent conversations today facilitate easier administration and healthier family dynamics down the road.

When should a blended family update its estate plan?

Review and update your plan after major life events: marriage, divorce, birth or adoption of a child, death in the family, large financial changes, or relocation. Most professionals suggest at a minimum checking in every 3 to 5 years to verify your intentions and legality.

How can we avoid conflict between stepchildren and a surviving spouse?

Utilize thorough paperwork, clear inheritance directives and, when needed, distinct spouse and children’s trusts. Name neutral fiduciaries and document your logic. Mix this with open dialogue during your lifetime to minimize confusion and court battles.

Need help beyond this topic? Nigro Manucci LLP provides trusted legal guidance for individuals and businesses across Alberta in real estate, corporate law, and estate planning.

Residential Real Estate Transactions

For official legal information and court procedures in Alberta, explore these trusted resources: