- Key Takeaways

- The Closing Process Unpacked

- Key Players and Their Roles

- Understanding Closing Costs

- Common Closing Pitfalls

- The Digital Shift in Closings

- Why Legal Counsel is Crucial

- Conclusion

- Frequently Asked Questions

Key Takeaways

- Consider closing as the last legal hurdle to transfer ownership and strategize to hit every deadline. Have papers, ID, and verified funds on hand prior to this date.

- Due diligence early can save a real estate closing. Arrange a title search, examine disclosures, arrange inspections, and verify insurance and contingencies.

- Work closely with everyone to keep things moving. Keep the buyer, seller, agent, lender, and lawyer in communication to solve issues fast.

- Nail mortgage approval with complete paperwork and early check-ins. Verify loan terms, signing needs, and when funds will be released prior to closing day.

- Go over fees and statements to avoid surprises. Verify that legal fees, property tax adjustments, title insurance, and other prorations are correct on the closing statement.

- Use digital tools to eliminate steps where possible. Make sure e-signatures, virtual meetings, and secure portals are legal and secure, which cuts down on errors and saves time.

Real estate closing is the last step in a property sale during which the ownership transfers from the seller to the buyer. This means signing the deed, loan papers, closing costs, and recording with the local office. Buyers typically bring photo ID, proof of insurance, and a cashier’s check or wire. Lenders ship a Closing Disclosure with fees, including appraisal, title search, and taxes. Title companies or attorneys are escrowing, checking liens, and clearing holds. A final walk-through verifies that negotiated repairs have been completed and that the home is in the same condition. Money is available after forms are signed and filed. To help set expectations, the guide below details each step, typical fees, and timelines.

The Closing Process Unpacked

It’s the legal transfer of property from seller to buyer. It depends on deadlines, clear documentation, secured financing, and efficient collaboration between buyer, seller, attorneys, lenders, and brokers. Title checks and document reviews eliminate last minute risk.

1. The Accepted Offer

We both sign the purchase agreement to lock in price, terms, and a target closing date. Review the calendar today. Missed dates can sabotage financing or trigger penalties.

Check your contingencies closely. Typical ones are inspection, financing, appraisal, and sale of the buyer’s existing home. If an inspection uncovers roof leaks or unsafe wiring, bargain for repairs, credits, or a price adjustment in writing.

Put down good faith money into a neutral escrow. That demonstrates good faith and is later credited to the price or closing costs. Keep deadlines on track with a shared checklist so appraisal ordering and disclosure review don’t slip.

2. Due Diligence

Schedule a comprehensive home inspection and if necessary, targeted inspections for termites, foundation, or environmental hazards. Take the report and use it to set repair requests or budget plans.

Be sure to look for liens, claims, or easements like a utility line across the yard and run a title search. Repair issues with lien releases or title insurance endorsements. Go over seller disclosures and check them against what you witnessed during visits. Make sure any promises like appliances are in the contract.

Buyers should obtain property insurance that satisfies lender criteria and local risk, including flood coverage if necessary.

3. Mortgage Approval

Provide income verification, bank statements, IDs, and asset documents in order for the lender to generate final approval. Understand the loan’s interest rate, term, prepayment penalties, and monthly payment.

Coordinate with lender on necessary appraisals and conditions to release funds at closing. Go over and sign loan documents before that date to prevent delays.

4. Legal Formalities

Lawyers draw up the deed, transfer forms, tax documents, and affidavits. Verify names, legal descriptions, and amounts correspond with the contract and lender numbers.

Sign with appropriate witnesses and notarization as required by local law. Have legal fees and transfer taxes calculated and ready to go.

5. The Final Review

Conduct a final walkthrough to verify condition, repairs, and inclusions. Make sure all contract requirements are fulfilled. Go over the closing statement line by line for prorations, taxes, and fees. Make sure any necessary documents are collected and signed.

6. The Transfer

The lawyer records title with the land registry. The lender or escrow releases funds to the seller after recording. Keys and possession transfer on the date agreed upon, and both parties receive proceeds and complete closing copies.

Key Players and Their Roles

Real estate closings combine the key players to transfer money, verify ownership and transfer title. Roles differ by state or locality, and some locations require an attorney or escrow agent at closing. Defined responsibilities, fast responses, and tidy documentation keep deadlines on schedule.

The Buyer

Buyers queue up cash in advance. We’re talking mortgage pre-approval, final loan approval, and cash for closing costs, taxes, and reserves. If cash is used, proof of funds is required well before signing.

They handle due diligence by scheduling inspections, ordering a survey if needed, reviewing the purchase agreement, and reading every closing document. They inquire about loan terms, rate lock, and any prepayment policies.

A walkthrough to finalize and ensure that the home’s condition is as agreed upon. Test fixtures, note repairs, and check that agreed items stay.

When closing, purchasers sign the note, mortgage or deed of trust, disclosures, and title/settlement papers. Once funds disburse and documents record, they are the legal owner.

The Seller

Sellers complete all of the terms in the purchase agreement, such as agreed-upon repairs, credits, or disclosures. Save receipts, permits, and warranties.

They have to provide a clean title. That could include paying off liens, addressing boundary disputes, or eliminating unpaid fees. A title insurance company will identify defects and repair them quickly.

Prep for handover: remove personal items, leave keys and codes, and vacate by the set date. Clean to a reasonable degree.

Sign the deed and transfer paperwork. Verify payoff and wiring details with the closing agent to prevent fraud.

The Real Estate Agent

Agents or brokers work out the purchase agreement and keep everyone on the same page, from the closing or escrow agent to the mortgage lender. They monitor inspection, financing, and document deadlines.

They outline actions, highlight dangers, and assist customers in evaluating decisions such as repair credits versus price reductions. If problems arise, like low appraisal, survey gap, or slow condo docs, they spearhead solutions and shift deadlines where possible.

The Mortgage Lender

Underwriters check income, debts, assets, and value and clear to close. They finalize loan documents and transmit the closing package to settlement.

They wire funds in a timely manner to the closing or escrow agent. All loan contingencies, including insurance, valuations, and final credit check, need to be in before the closing date.

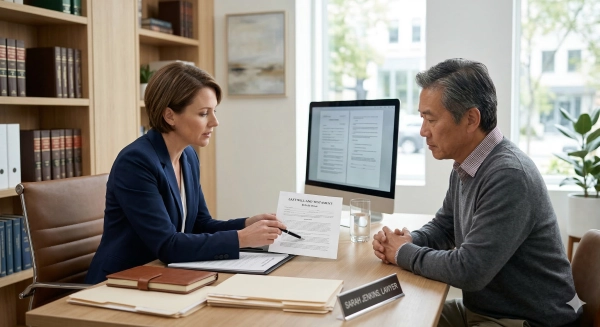

The Lawyer

Attorneys fine tune contracts and closing documents, bring everything in line with local law and define risks. Some states require an attorney to conduct or attend closing.

They conduct or examine the title search, remedy imperfections, and describe title insurance coverage for the purchaser and lender. They orchestrate the fund flow, deed recording, and ensure that all legal processes wrap up in the correct sequence.

Closing/escrow agent – This is a neutral third party that collects signatures, escrow funds and actually closes the settlement. If delays arise, close coordination among the agent or broker, the closing agent and lender can keep the deal moving.

Understanding Closing Costs

Closing costs are the closing fees due when a home sale is completed. They include fees for attorneys’ work, taxes, insurance, lender fees, and prorations. Usual totals are between 3% and 6% of the purchase price. Many buyers reserve at least 1.5%, but 4 to 5% is safer. Consider property transfer tax, appraisal, escrow deposits, and prepaid interest. Examine the closing statement line by line to prevent unexpected fees.

- Property transfer tax is based on fair market value and is usually a top cost.

- Legal fees for document prep, registration, and advice

- Title insurance (owner and/or lender policies)

- Appraisal fee (often starts near $350)

- Lender fees and underwriting charges

- Escrow deposit (often two months of tax and insurance)

- Prepaid interest to first payment date

- Property tax and utility adjustments

- Condo fees and homeowners’ association dues

- Courier, registration, and small admin charges

Buyers should expect condo fee prorations, prepaid utilities and meter balances. The national average in 2021 was around $6,905 with transfer taxes or $3,860 without them.

Legal Fees

Legal fees include contract review, drafting of documents, title search and registration, and any legal counsel associated with any risk, liens, or encroachments. Generally, firms charge a fee on a base plus disbursements for searches, certificates, and registrations.

Compare fees. Question what’s included, what counts as a disbursement, and what triggers additional time. Ask for an itemized invoice that details each task and third-party expense. Legal fees are typically paid on closing day through the closing statement.

Property Taxes

There are property tax adjustments that divide the year’s taxes so that each party pays for the days that they owned the home. The closing statement displays a prorated portion. Verify the dates, rate, and any local levies.

Make sure all back taxes are paid before closing so there are no liens. Once it’s transferred, make sure to update tax records with the local taxing authority so that bills and notices are sent to the new owner.

Title Insurance

Title insurance protects you from losses due to defects or disputes in ownership, such as unknown liens or boundary issues. Buyers buy a policy at closing and lenders tend to want one, too.

Learn about coverage, exclusions, and how to file a claim. This one-time premium provides security to both the buyer and the lender.

Other Adjustments

- Utilities: Water, power, and gas are based on meter reads or estimates.

- Condo/HOA: dues, special assessments, move-in fees, or reserves.

- Fuel: heating oil or propane by measured volume.

- Rent: if tenants stay, split rent and deposits fairly.

Confirm every figure on your closing statement. Flag any mismatch prior to signing. These adjustments maintain ongoing costs that are equitable to both parties.

Common Closing Pitfalls

Frequent sources of delay or stress and how to avoid them:

- Missing documents: confirm IDs, proof of funds, insurance, and lender forms early.

- Financing gaps: lock rate, track lender milestones and meet cut-off dates.

- Title concerns: Clear liens, confirm easements, and resolve ownership gaps fast.

- Survey issues include using a licensed survey and avoiding sketches or online maps.

- Inspection fallout: Set deadlines, define scope, and agree on repairs or credits.

- Document errors: verify names, dates, amounts, and legal descriptions.

- Communication lapses: Respond within 24 hours, log updates, and confirm in writing.

- Cost surprises: Model closing costs, taxes, and repairs to avoid shortfalls.

- Timeline drift: Align all parties on a shared calendar and reminders.

Financing Delays

Closing delays due to incomplete mortgage files and missed lender deadlines. In other words, stay in frequent contact with the loan officer and request a timeline with target dates for appraisal, underwriting, and final approval. Update the agent and lawyer so all can catch risks early.

Mail requested documents the same day—pay stubs, bank statements, tax returns, gift letters. Tiny gaps cause re-underwriting. Don’t open new debt, new jobs, or make large cash moves prior to close. This can throw off your approval and even change your rate. When days count, delayed responses undermine trust and endanger the deal.

Title Defects

Liens, unpaid assessments, boundary encroachments, easements without recorded rights, or heir disputes can block a clean transfer. Many sellers try to use blueprints, subdivision sketches, or map screenshots as “surveys,” which invites conflict and delay.

Don’t you lawyers open title early, order a licensed survey, and start curative steps at once? Buyers should read the title report, identify exceptions, and inquire about what each one means in laymen’s terms. Title insurance doesn’t protect against latent, undisclosed defects, so discover them before funding, not after.

Inspection Surprises

Checklist:

- Include a home inspection contingency complete with a three-day professional review and resolution steps.

- Before the deadline, negotiate repairs or credits. Who writes the scope, cost, and who pays?

- To minimize post-close claims, sellers must disclose known defects.

- Reread inspection and survey results line by line. Miss about common closing pitfalls.

Unaccounted delays, ambiguous reporting or last-minute requests for repairs should be handled quickly before they snowball.

Document Errors

Incorrect names, dates, prices or tax can halt a signing. Get them all to pre-read drafts 48 hours in advance. Attorneys need to verify legal descriptions, parcel IDs, and registration information. Things to avoid at the close. Sellers who are hung up on price tend to overlook cost items such as closing fees, taxes, and repairs that can result in a cash shortfall on closing day.

The Digital Shift in Closings

The digital shift in closings Digital tools now manage pivotal steps in real estate closings, from meetings to signatures to file exchange. The goal is simple: cut delays, reduce errors, and keep clients safe while they move fast. With average satisfaction scores of 4.97 out of 5, that lines up with what clients value: less travel, fewer strict requirements, and an easier journey to the finish.

Virtual Meetings

Closings go digital. Video calls supplant lots of in-person visits to consult, check IDs and walk through closing packets. Buyers in a different city can go over the statement of adjustments, make inquiries live and view screen-shared drafts prior to signing.

Schedule sessions around real life. Weeknights or weekends are okay so folks with late shifts or parent duties can participate. This is a definite departure from the old model that required midday office runs.

Have everyone establish a reliable internet connection, a private location, and a camera-enabled device with an active microphone. If one side has limited access, put in a backup by phone and share read-only files to stay on track without jeopardy.

Electronic Signatures

E‑signatures are valid for most closing papers — offers, amendments, disclosures, and many lender forms, subject to local law. Use platforms that track time stamps, IP data, and audit trails.

Choose tools with multi-factor login, tamper-evident seals, and transparent identity verification. Your lawyer or notary can tell you which forms still require wet ink, such as certain notarized deeds or jurisdiction-specific affidavits, and can arrange for a remote online notarization if permitted.

E-signing reduces turn times, prevents re-printing, and eliminates typical errors like missed initials. It empowers out-of-town buyers to sign from home without any travel.

Secure Portals

Utilize encrypted portals for IDs, bank letters, payoff statements, wire details, and final reports. Don’t email wiring instructions! Upload documents within the portal, verify the payee, and call the established office number ahead of any transfer.

Enable alerts, then review notifications for to-dos, comments, and signature requests. With automated forms and real-time sync, teams view the same file, edit once, and avoid version drift. This minimizes manual input and streamlines lender and title checkers.

Portals reduce fraud potential and maintain access role-based. Some services run widely, with concentrations in Ontario and Alberta now and expansion ahead, indicating the model is not geographically locked.

Why Legal Counsel is Crucial

| Role | What the Lawyer Does | Why It Matters |

|---|---|---|

| Contract review | Reads the Agreement of Purchase and Sale, flags vague or risky clauses, explains duties and deadlines | Prevents misunderstandings and hidden traps that can cost money or delay closing |

| Title search | Confirms legal ownership, checks liens, easements, encroachments, unpaid taxes | Avoids property loss, boundary fights, or debt you did not agree to |

| Condition tracking | Verifies financing, inspections, repairs, and other conditions are met or waived in time | Reduces risk of breach and last‑minute cancelations |

| Compliance check | Ensures the deal aligns with local laws, lender rules, and disclosure standards | Cuts legal exposure and keeps lenders satisfied |

| Funds and payouts | Confirms wire details, trust accounting, and correct disbursements to seller, lenders, and tax bodies | Protects against wire fraud, errors, or missing credits |

| Closing coordination | Aligns buyer, seller, agents, and banks; prepares statements and closing package | Keeps closing day smooth and avoids costly delays |

| Post‑closing steps | Registers transfer and mortgage, releases holds, delivers final records | Secures ownership and prevents future title issues |

Lawyers assist in mitigating expensive errors. For instance, a phrase such as ‘repairs to be completed’ with no apparent list can ignite a conflict. A lawyer will request a dated repair addendum with receipts and verification of completed work. If a title search reveals a lien from a previous contractor, counsel can withhold funds until it is cleared. If an easement restricts building height, they will describe how it impacts future plans. This is particularly vital when purchasing a house, which for most individuals is the most significant and costly decision they make.

Legal counsel safeguards each financial move. They verify closing numbers, the statement of adjustments, and trust transfers prior to disbursement. On closing day, they coordinate with lender instructions, verify insurance is in place, and make sure all signatures are executed properly.

For readers in Sherwood Park and throughout Alberta, Nigro Manucci provides real estate closing assistance that’s reliable and transparent. They lead you through document preparation, title review, lender and agent coordination, and easy transfer and registration, so you fulfill all obligations under the agreement and close with less anxiety.

Conclusion

TRANSPARENT PATH TO CLOSE Save time and cut stress and fees with a transparent path to close. Understand the process, understand the fees, and understand who performs which tasks. That combination provides you control.

HOW DO YOU KEEP YOUR DEALS ON TRACK? For instance, verify wire information by phone with the bank and title office. Catch title issues early with a complete report. Request a fee sheet from your lender for every line item. Easy steps lead to actual profits.

Digital tools accelerate procedures and minimize mistakes. E-sign, e-notes, and remote notarization can assist if your jurisdiction permits.

Looking for a next step? Consult a real estate lawyer or trusted agent today. Have a clean close.

Frequently Asked Questions

What happens during a real estate closing?

Closing is the last step. You sign papers, pay closing expenses, and wire money. The deed is recorded and ownership is transferred. Anticipate ID checks, a review of the final numbers, and confirmation of keys or entry access. Generally, closings can take one to two hours if the documents are all in order.

Who are the key players at closing?

Usual suspects are the buyer, seller, the real estate agents, lender, closing agent or escrow officer, and occasionally an attorney. Title company people might come as well. All parties review paperwork, finances, and legal requirements to complete the transaction.

What are typical closing costs?

Closing costs generally fall between 2% and 5% of the purchase price. They encompass lender fees, title insurance, escrow fees, taxes, and recordings. You can prepay insurance and interest. Request a complete itemized estimate before closing.

How can I avoid common closing pitfalls?

- Begin with a simple checklist.

- Don’t open new credit.

- Confirm wire instructions by phone.

- Verify your Closing Disclosure ahead of time.

- Verify ID and insurance.

- Arrange a final walk-through.

- If needed, bring certified funds.

- Have your agent or attorney pre-check papers.

Are digital or remote closings secure?

Yeah, done through respected providers. RON and e-signatures come after rigorous identity verification and encryption. Just make sure your state or country permits it. Check portals and wire instructions always. Digital closings can minimize mistakes and accelerate funding.

Do I really need a real estate attorney?

One thing that an attorney does is protect your legal and financial interests. They review contracts, resolve title issues, and clarify risks. This is important for intricate transactions, specialized listings, or regional legal needs. A quick consult can save expensive errors.

When should I review the Closing Disclosure?

Go over it immediately, preferably three days prior to closing. Review your loan terms, interest rate, cash to close, and fees. Compare it to previous projections. Notice any discrepancies right away, so your lender and closing agent can fix them.

Not what you were looking for? Explore Nigro Manucci’s trusted legal resources and services for businesses and individuals across Alberta.

Shareholder Agreements Alberta

If you’d like to explore additional information about business law and regulations, these trusted sources may be helpful: